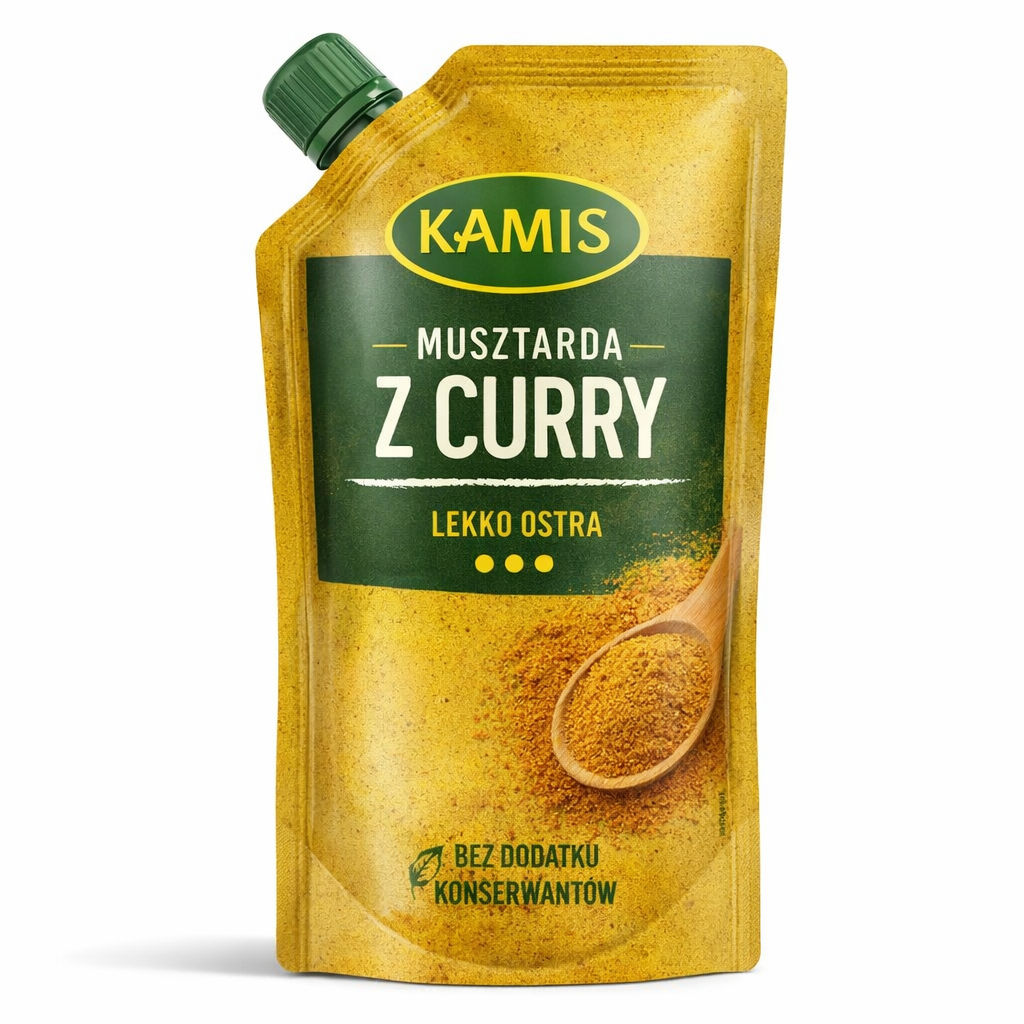

Visiting a store this week, I saw the first real sign of spring in FMCG: BBQ displays are back.

But something specific here caught my attention.

We are witnessing a shift from family-size formats to single-occasion packaging.

Think about a typical BBQ setup:

paper plates, cutlery

sauces

a large jar of mayonnaise, mustard and a bottle of ketchup, a BBQ, barbecue sauce, Thousand Island dressing…

Imagine the last point. All those jars and bottles.

It is heavy to carry it. It is expensive one-time-cost – inflating the bill of BBQ.

After party is over the question come- who takes the leftovers home? No one wants it, no one feels comofrtable to put it into trash.

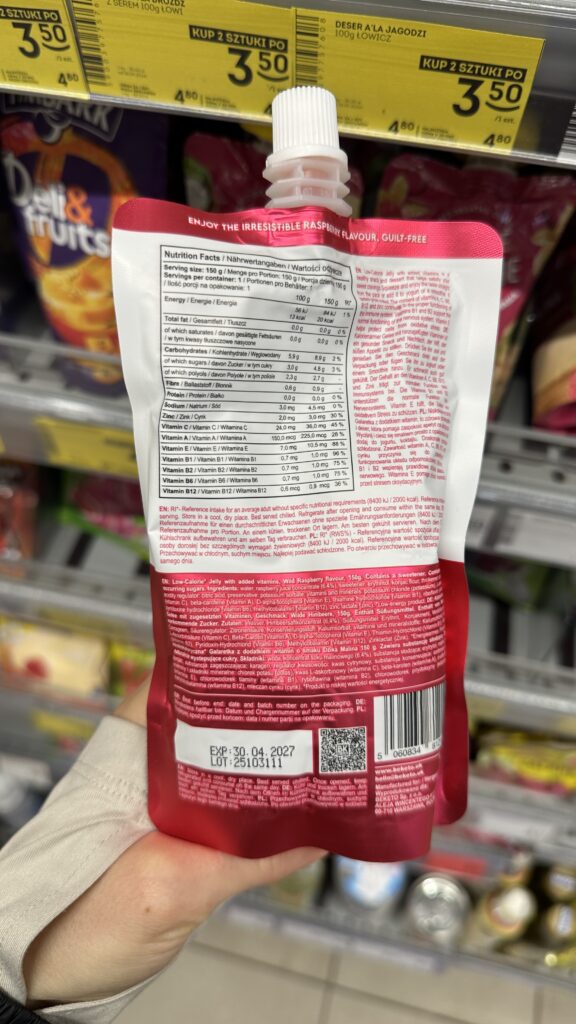

500g ketchup suddenly becomes a problem, not a solution. It’s inefficient, wasteful. This is where pouches come in.

UX is quietly winning

Traditional rigid bottles are a design from another era.

We all know the moment: the ketchup is “finished”… but not really. You shake, you hit, you squeeze — and still leave 10–15% inside.

Pouches solve this perfectly:

full evacuation of product

intuitive usage (like toothpaste)

no frustration at the end

It’s not just packaging. It’s experience design.

And in FMCG — UX is becoming king again.

BBQ is just the beginning

Single-use or single-occasion pouches make perfect sense for:

ketchup, mayo, sauces

marinades

oils & dressings

They remove friction:

no leftovers

easy cost-sharing

less waste

light to carry

spoon not needed

This is not just convenience. This is context-based packaging — designed for the moment of use.

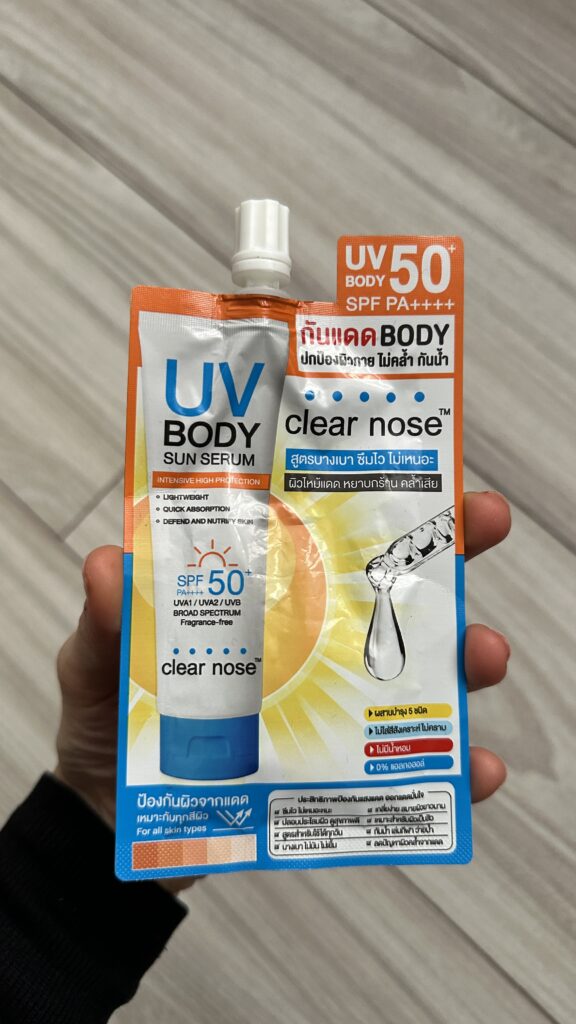

Asia already figured it out

Travel a bit, and you’ll see how far this can go.

In many Asian markets, pouches are not a niche — they are a default format, especially in cosmetics.

Seven Eleven Store

And this is where it gets really interesting.

My personal favorite example: SPF cream in a pouch.

Why it works:

zero leakage risk

lightweight

flexible — fits anywhere

perfect for daily carry

It removes the biggest barrier to usage: inconvenience.

With such product something annoying (carrying heavy bottle of SPF protection) becomes less friction act (small product that I can always have with myself and protect skin).

While the world is currently obsessed with the soft pinks of Japan’s cherry blossoms, the FMCG aisles are blushing a very different color: Matcha Green.

It feels as though we’ve blinked and the “Pistachio Fever” of last year has been seamlessly swapped for a “Matcha Obsession”. It is nearly impossible to navigate a store today without spotting a “green innovation” on every second shelf.

The formula for a 2026 hit seems deceptively simple:

take your bestseller,

add a dash of matcha,

wrap it in forest-green branding,

…and watch it fly. Voilà!

Let’s look at who is winning the green rush and where matcha actually makes sense but hasn’t arrived yet.

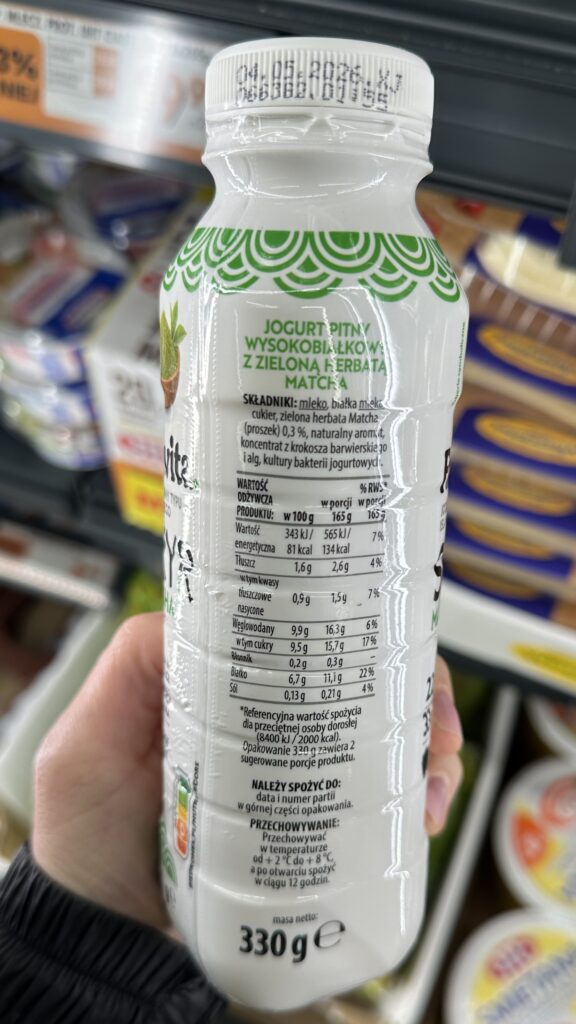

Skyr Drink

The combination of a high-protein Icelandic-style yogurt with this specific tea infusion is a brilliant move that targets the “modern achiever” persona—someone looking for functional health benefits (high protein) and a mental boost in a convenient, on-the-go format. While the packaging design maintains a clean, typical of Biedronka’s private label, the highlight of 22g of protein justifies the price point for the Polish market, where high-protein dairy remains a premium-yet-accessible staple for health-conscious consumers. This product successfully bridges the gap between a traditional snack and a functional supplement, making it a highly relevant addition to the competitive “fit” segment of local retail shelves.

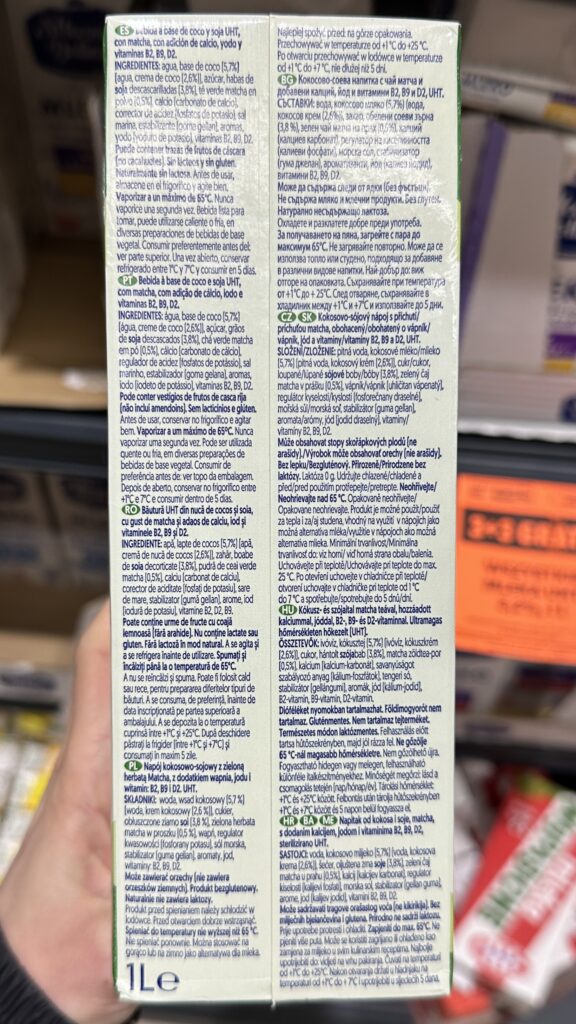

2. Plant Based Drink

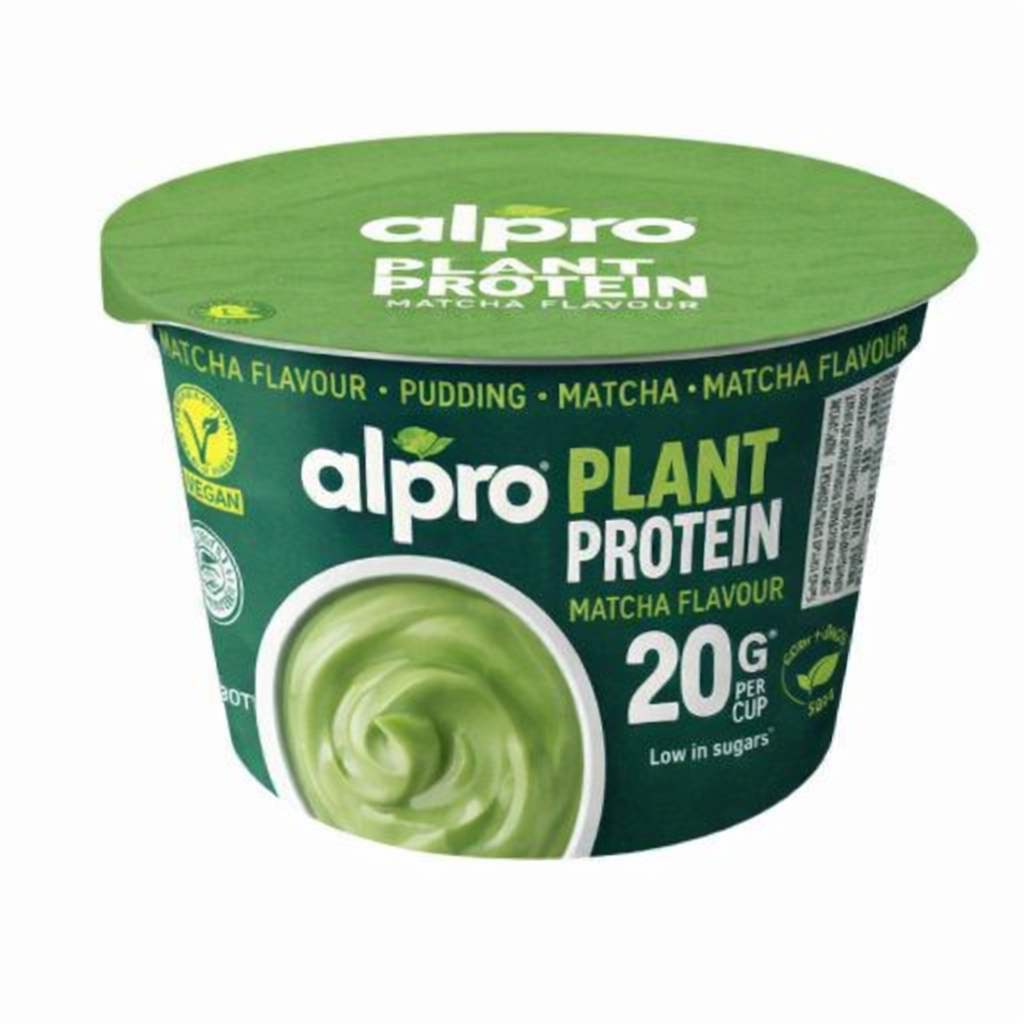

This is a calculated move by Alpro to dominate the “home-barista” segment, offering a foamable, ready-to-drink solution that eliminates the hassle of manual mixing for the urban Gen Z and Millennial target who value aesthetic, plant-based lifestyle rituals. The vibrant, clean packaging design perfectly signals freshness and high-tier positioning. The product’s strength lies in its versatility—being equally functional for iced Summer drinks or hot lattes—making it a sophisticated, staple for the modern health-conscious pantry.

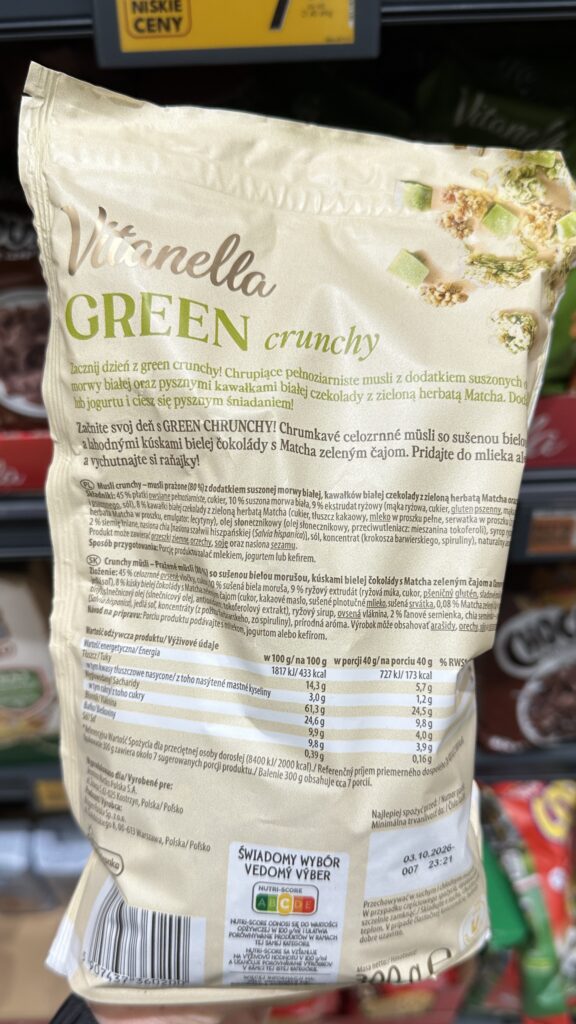

3.Muesli Crunchy

The inclusion of white chocolate with matcha and dried white mulberry in this crunchy granola creates a unique flavor profile that elevates a standard breakfast category into a more dessert-like experience. The soft green and cream packaging design effectively communicates a “natural” yet indulgent identity, standing out on shelves while maintaining the approachable brand recognition. Priced at 7.49 PLN for a 300g-350g bag, this product offers excellent value for the Polish market, successfully democratizing a trendy, cafe-style flavor combination for the mass consumer.

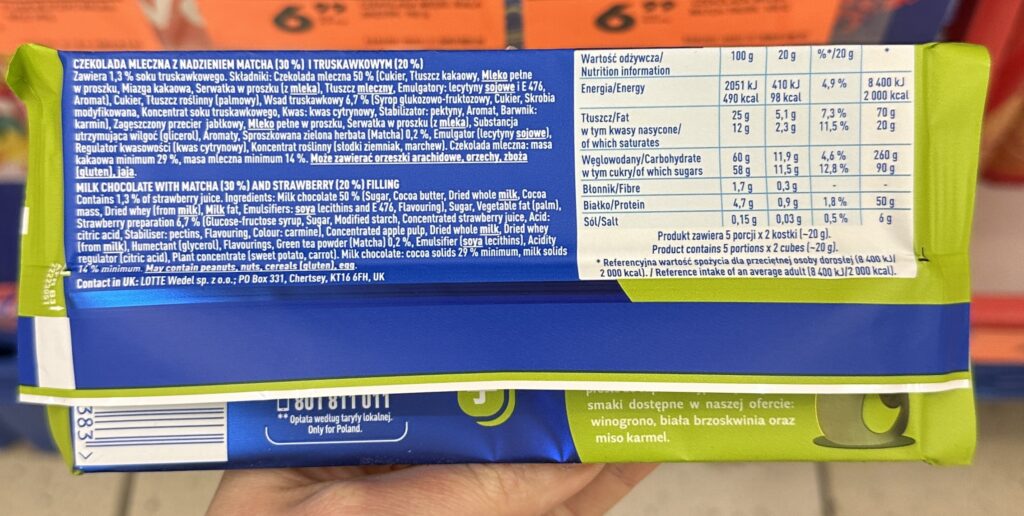

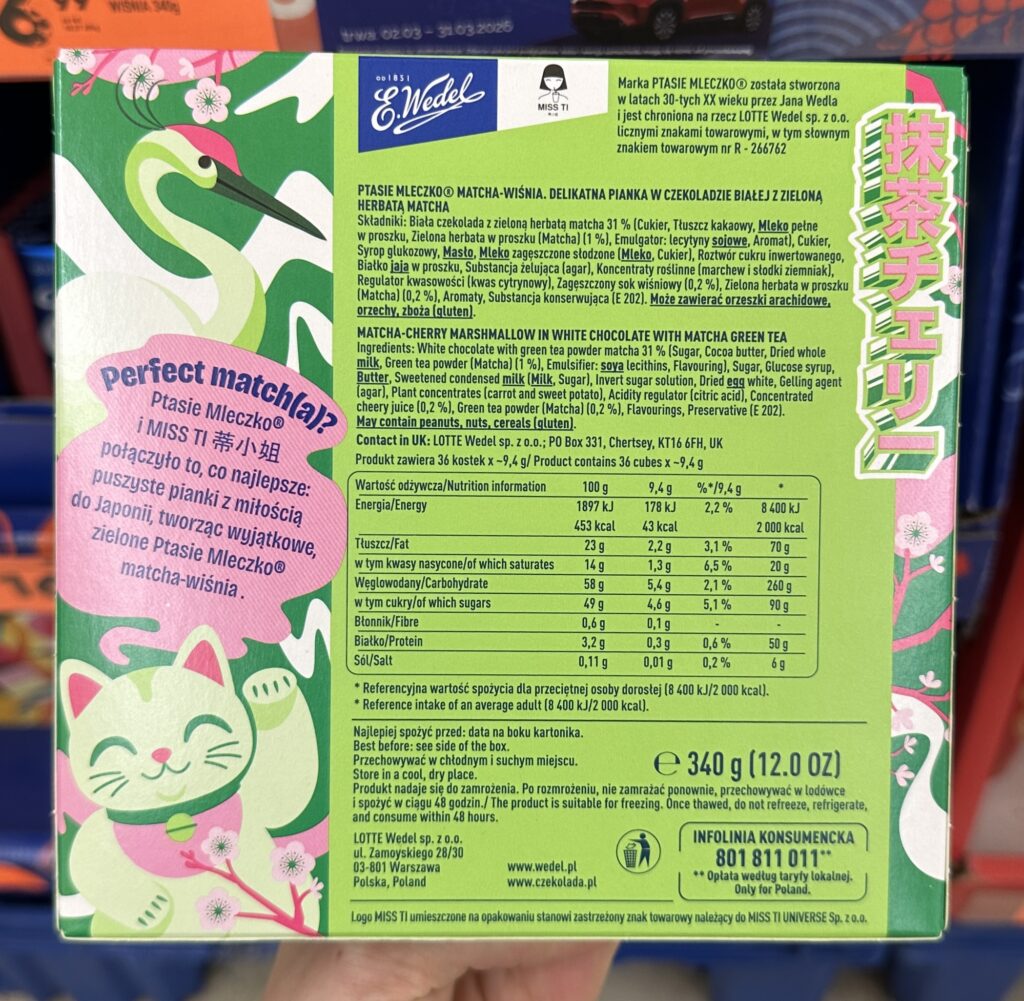

4. Chocolate table

E. Wedel’s limited-edition fusion of milk chocolate with strawberry and matcha filling is a masterclass in “oriental-chic” marketing, successfully blending traditional chocolate table with a trendy Japanese-inspired aesthetic. The packaging design is exceptionally vibrant, using pop-art illustrations and Maneki-neko motifs.

At a price of 6.99 PLN, it is positioned as an “affordable luxury” impulse buy, offering a high-perceived value that justifies the slight markup over classic flavor variants.

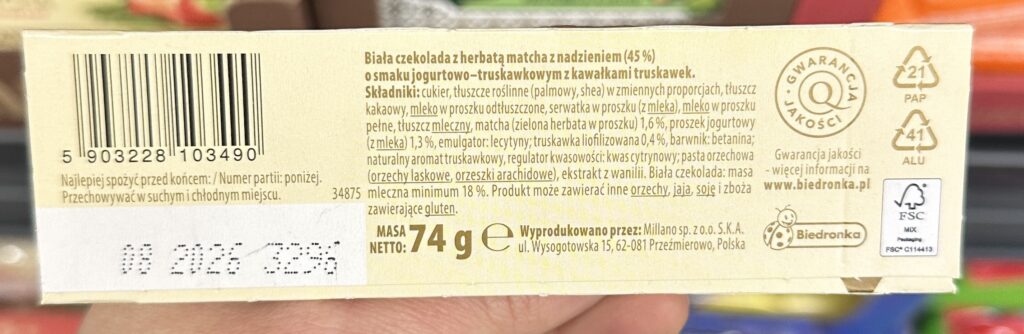

5. White Chocolate Bar

The pairing of a white chocolate-matcha shell with a yogurt-strawberry filling makes perfect sense as it balances earthy bitterness with creamy acidity, specifically targeting the price-sensitive “lifestyle explorer” as this is private label product. Carton remains in neutral colours, only “green” element is product display at the front. Given the 74g it is almost same as the traditional chocolate tables.

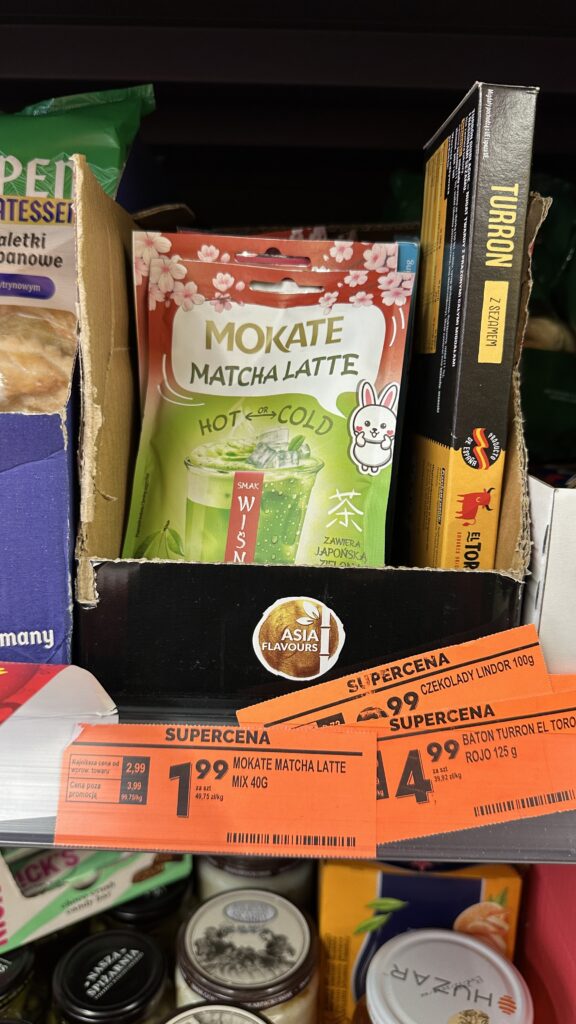

6. Matcha itself

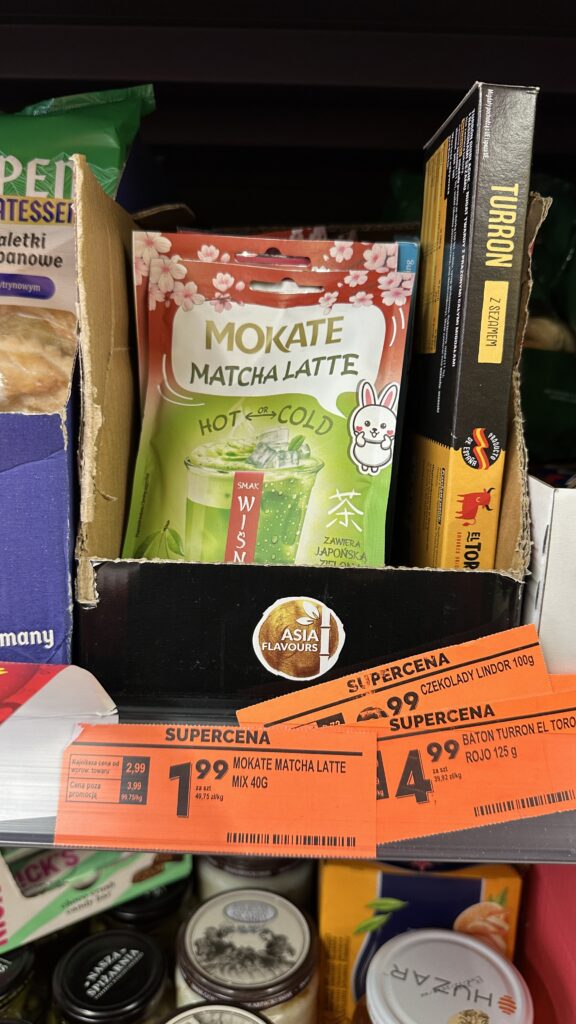

This is a smart market entry for Biedronka’s private label, offering a low-barrier way for mass-market consumers to experiment with trending café flavors at home without requiring specialized equipment or expensive milk alternatives. The target persona is a budget-conscious Gen Z or Millennial shopper who follows global wellness trends but prefers the convenience and pricepoint of a discount supermarket over a specialty coffee house. This product is highly reasonable for the Polish reality, as it offers a “luxury” café experience for a fraction of the 20+ PLN price per serving often found in cities like Warsaw. The packaging design is effective, utilizing “Kawaii” aesthetics and cherry blossom motifs to signal lifestyle appeal, while clearly communicating versatility through “Hot or Cold” preparation icons.

7. Soufflé Chocolates

This product successfully bridge the gap between a beloved Polish tradition and the modern “functional flavor” trend, though its execution leans heavily on visual novelty. The target persona is clearly the younger, “online” consumer who values aesthetic novelty, making the 16.99 PLN price point a reasonable “treat” for a limited-time experience. However, the packaging design is visually chaotic; it attempts to blend too many disparate elements—classical heritage branding, anime illustrations, and high-contrast color blocking—resulting in a cluttered hierarchy.

8. Matcha drink

This product is clearly designed for the “impulse buy” section, utilizing a logical yet nutrition-poor combination of instant flavoring and convenience that targets young, trend-driven shoppers looking for a “trend” rather than health benefits. Low entry price of 1.99 PLN—a highly reasonable, almost disposable cost for the Polish market, however, notice it is only 1 portion. Also, disappointing reality: with only 4% actual tea content and a primary ingredient list of sugar and glucose syrup, the “wellness” promise of the tea category is completely overshadowed by a synthetic, high-calorie profile that prioritizes shelf-stable sweetness over quality.

The design is a textbook example of “visual indecision”, creating an aesthetic clash by placing a hyper-realistic cherry photo alongside a simplified cartoon bunny and traditional Japanese calligraphy. The red-and-green color scheme, while intended to represent the cherry flavor, leans dangerously close to a “tomato juice” palette, which fails to harmonize as effectively as a pink-and-green “sakura” theme would.

9. White chocolate table

This product is a “premium-wash” specialty chocolate that successfully uses a sophisticated flavor combination to mask a relatively low inclusion rate of its headline ingredients, making it an excellentmargin-driver for the manufacturer. It targets the “affordable luxury” persona—likely a middle-class shopper looking for a sophisticated evening snack or a quick self-indulgent purchase—who is easily swayed by the elegant, minimalistpackaging featuring gold foil lettering and clean typography. While the design looks high-end, the reality is a classic case of marketing inflation, as the 30% price markup over standard chocolate is built on just 2% low-quality powder and a tiny fraction of fruit.

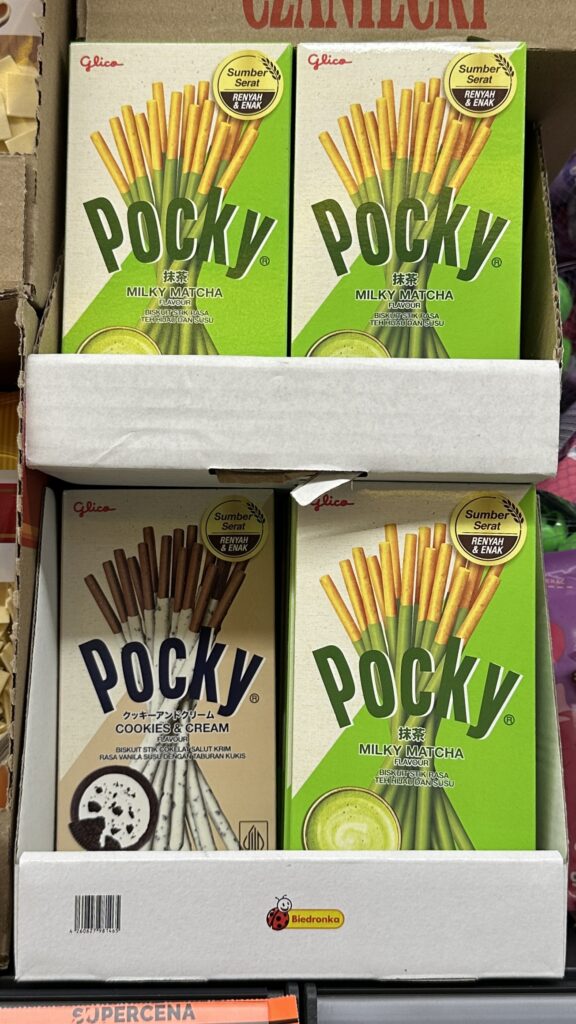

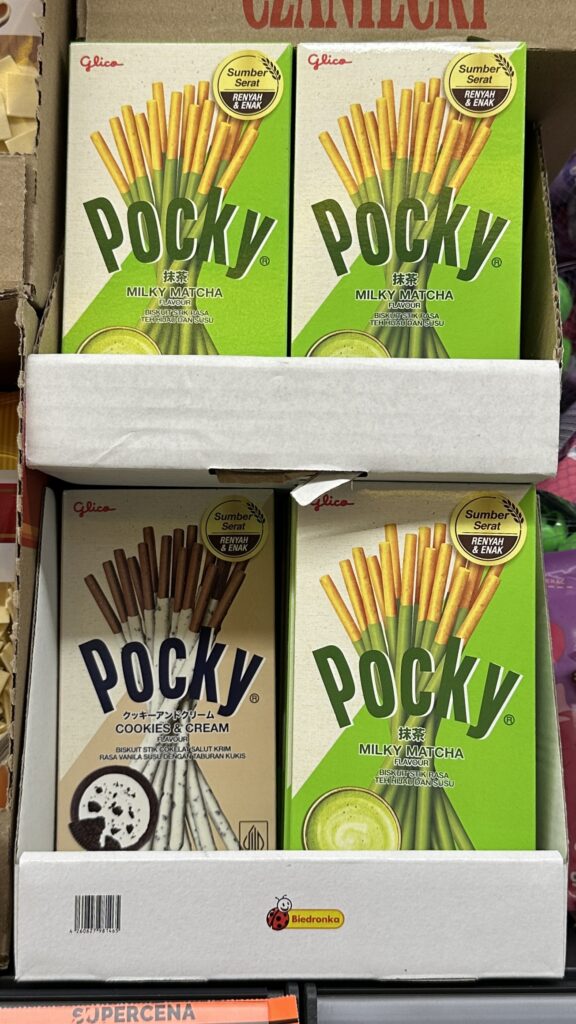

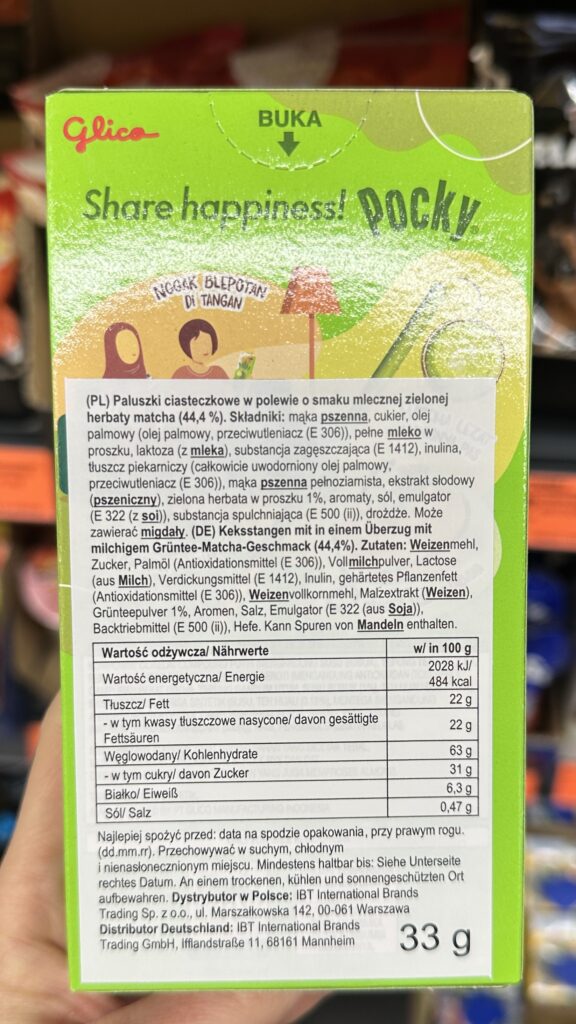

10. Chocolate cookie sticks

While Pocky is an iconic global snack, this version featuring a matcha profile is a textbook example of a “global curiosity” product that feels somewhat out of place in a standard Polish discount aisle due to its hyper-localized Southeast Asian branding. The combination of a crunchy biscuit with a sweet, grassy coating is a proven winner for the “snack-adventurer” or K-pop/J-pop fan.The pricing for such a small “import” item remains a premium compared to local snacks.

Where are still opportunities

I see multiple opportunities to use this matcha trend to win in multiple categories.

First what come to my mind is dairy/plant-based desserts. Relatively easy to achieve, fast moving good, ideal to adopt to seasonal matcha trend.

My top pick? Monte. It captures that sweet spot of Gen Z nostalgia while refreshing the profile for a more “grown-up” palate.

My next bet on easy-to-create, easy-to-bring-to-market products would be pouches.

Currently I think there is missing piece on bars which are known well but in a seasonal limited edition witch matcha flavour.

Soon, we start ice cream season – another segment that is just waiting to hit with green energy.

Summary

The “Green Rush” of 2026 is more than just a color shift on the shelves; it is a litmus test for agility in the FMCG sector.

The winners will be the brands that successfully integrate matcha’s earthy profile into a functional benefit—like the high-protein Skyr—or those that leverage deep-seated emotional triggers.

What’s Next?

As we navigate the rest of the year, keep an eye on the “chilled zone.” This is where the highest velocity meets the highest trend-sensitivity. If you aren’t already planning your seasonal LTO (Limited Time Offer) around a balanced, high-quality matcha flavor, you’re leaving shelf space to the competition.

Is matcha a permanent staple or a passing cloud? In the world of fast-moving consumer goods, the answer doesn’t really matter as long as you are the first to the checkout zone with a product that resonates. The “Green Obsession” is here for now—it’s time to make it work for your margins before new trend will kick in.

Walk into a typical discount or grocery store in Poland today and something feels off almost immediately. Not because of pricing (maybe this can hit you if your last visit in PL was in 2003), not because of assortment—but because of space. Or rather, the lack of it.

Aisles are no longer corridors designed for flow; they have become obstacle courses. Cardboard displays rise unexpectedly at every turn, clip strips hang into walking paths, and promotional towers compete for every available square meter. The shopping act, once routine and almost automatic, turns into a careful navigation exercise.

We often talk about the “Golden Zone” on a shelf, but in many Polish stores, the floor has become the new battlefield. When you see temporary displays (FSDUs/shippers) blocking every turn, it’s usually because the store manager is caught between two fires: HQ-negotiated contracts that mandate these displays and a “backroom” that is already overflowing.

The sense of chaos is a psychological “stop sign” for shoppers. When a shopper has to physically protect their body or bag from knocking over a tower of energy drinks, their cortisol levels rise. A stressed shopper buys only what is on their list and flees, which is the exact opposite of what an extra exposition is supposed to achieve.

The Fridge vs. Ambient Paradox

Let’s look at UHT milk or ambient beverages. Chilled square footage is the most expensive “real estate” in a store due to electricity and maintenancecosts. Using it for products that don’t require it (just to get a “double hit” of visibility) is a massive inefficiency for the store owner. It limits the assortment of high-margin, short-shelf-life innovations like

plant-based yogurts

dairy products

fresh convenience meals

juices fresh-pressed

etc

The Clip Strip “Infection”

The next observation is every shelves covered with clip strip. Or rather clip strips. This is a symptom of “Micro-Space Greed.” These strips are designed for cross-merchandising (e.g., batteries next to toys). However, when they are everywhere, they become “visual noise.”

Taking the regular product from shelve without disruption is almost impossible. They are the first things to get knocked down, creating a look of a “discount graveyard” rather than a professional retail environment.

This is observation from just 1 visit in a small grocery store:

oatmeal

mini meringues (this packge is too large to hang this way!)

pet food

jelly beans and pet food (isn’t it affecting the quality of product?)

milky candies

crispy peanuts

lollipops

dried fruits

fabric stain remover and bread sticks (this shocked me! I wasn’t even considering such kind of product to hang on this display)

If you put attnetion in two of those examples we already see cartoon display blocking the shelve access (picture of milky candies and dried fruits)

Who Needs to Intervene?

This issue probably could be solved only by one of those:

The Fire Marshal (Straż Pożarna): This is the most immediate lever. Polish health and safety (BHP) and fire regulations are quite strict regarding the minimum width of evacuation routes. If a store’s “extra expositions” reduce a corridor below the legal limit (often 1.2m to 2.0m depending on the store size), they are in violation. More frequent inspections would force retailers to clear the “death traps” they’ve built out of cardboard and plastic.

Retail HQ (Category Managers): The “Commercial Team” needs to start talking to the “Operations Team.” Currently, HQ sells the floor space to producers without checking if the physical store can actually hold it. They need to implement “Display Caps”—a hard limit on the number of secondary placements allowed per square meter.

The Consumer (The Power of the Wallet): If shoppers move their loyalty to stores that prioritize “breathable” shopping the cluttered stores will see their “Time in Store” metric drop, which eventually forces a change in strategy. As pepole understimate the risk of potential accident due to overcrowd stores and they are looking for every opportunity to buy with lowest prices I think it is not likely to happened.

We are reaching a tipping point. What is gonna happened if stores continue to prioritize “temporary stimulus” over “basic navigation,”? Will they lose the modern shopper who values time and comfort over seeing the same UHT in four different places? Or lowest price will always win no-matter-what?

The collective packaging carton—often referred to as Shelf-Ready Packaging (SRP) or Retail-Ready Packaging (RRP)—has evolved from a mere shipping necessity into a critical touchpoint of the shopping act.

In modern retail, particularly within discounters like Aldi or Lidl, store staff rarely unpack individual units. Instead, the entire carton is placed directly onto the shelf. This means the carton is the “first face” the consumer sees. If designed poorly, it becomes a barrier; if designed brilliantly, it acts as a silent salesman that bridges the gap between a logistics necessity and a marketing powerhouse.

The primary function of any collective packaging is protection. It must safeguard the product through an impressive journey: from the high-speed vibrations of a factory conveyor belt to the stacking pressures in a Distribution Center (DC), and finally, the manual handling during store replenishment.

A carton that collapses under its own weight or tears during transit doesn’t just damage the product; it damages the brand’s perceived quality before a customer even touches it.

The engineering must ensure that every centimeter of corrugated board provides maximum vertical strength while remaining easy to open without any sharp tool, which could accidentally puncture the primary pouches inside.

The Human Factor – UX for Store Staff

We often overlook the “internal customer”—the store staff. If a case is difficult to grip, lacks clear “this side up” indicators, or has a perforated opening that requires a Herculean effort to tear, it will be handled roughly. Poorly designed cartons lead to “shelf-gore,” where jagged cardboard edges or half-torn flaps obscure the product.

A staff-friendly design includes intuitive hand-holes and “easy-open” features that allow for a clean, one-motion removal of the hood. When the staff finds a carton easy to work with, the product is more likely to be replenished promptly and positioned correctly on the shelf.

The Shopper’s Perspective: Frictionless Interaction

From a User Experience (UX) perspective, the carton must facilitate an effortless “grab-and-go” motion. We want to eliminate any physical tension at the moment of the buying decision!

If the front lip of the carton is too high, it hides the product itself, it is difficult to grab it quickly;

if it is too low, the products might tumble forward.

The ideal design uses a “low-cut” front that showcases the primary packaging while providing enough of a “tray” to keep the units upright and organized.

This ensures that even when the carton is half-empty, it doesn’t look like a chaotic bin of discarded items.

Marketing on the Edge: Eye-Catching Communication

The outer layer is prime real estate for marketing. In a sea of brown or white cardboard, color is your strongest weapon.

It should either match the brand’s core palette or provide a high-contrast backdrop that makes the product “pop.” Beyond aesthetics, the carton must communicate the “Reason to Buy” in large, legible fonts that can be read from two meters away.

Highlighting benefits like “No Added Sugar!” or “High Protein” on the tray lip reinforces the message on the pouch.

Furthermore, a strong Call to Action (CTA) like “Try Me!” or “New Flavor” can trigger an impulse purchase that the primary packaging alone might miss.

Analysis of Real-World Examples

Looking at the provided images, we can see a masterclass in both effective and missed opportunities in SRP design:

The Good: The Kubuś carton is a benchmark for effective SRP.

The bright green color perfectly aligns with the brand’s “natural/fruit” identity.

The tray lip is used strategically to scream “BEZ DODATKU CUKRU” (No Added Sugar). This is a critical benefit for parents.

The die-cut is clean, and the height of the front wall is perfectly calibrated—it holds the flexible pouches upright so the character’s faces are always visible, yet it doesn’t hide the product name. It utilizes every centimeter of the front-facing “lip” to communicate value.

The Bad: Pokett Fruit Bomb While the design of product itself seems to be modern, the execution of the collective carton leaves room for improvement.

The carton doesn’t give any message. The only thing included is the logo of the brand, that’s all.

Carton’s grey/brown color doesn’t make an eye catch; it is extremely boring in comparison to the product in exotic flavours. I would expect here something more “screaming”, maybe even neon color to give the product even more “exotic vibe”.

The Good: Panaflex This is a classic example of a “Value Pack” display.

The red“FAST ACTING IN 80 SEC” banner is a brilliant use of the shelf edge. It creates a secondary communication layer that sits below the product.

A lot of bad examples

Redundancy – Repeating the brand name 5 times in 10 centimeters. What’s the point?

Shadowing – High carton walls that turn products into “hidden treasures.”

Dead Space – Leaving huge % of the vertical shelf height empty and unbranded.

Lack of Hierarchy – No clear “hero” message, just a chaotic repetition of logos.

In conclusion, the collective carton is not just a box; it is a multifunctional tool.

To succeed, it must:

protect the goods,

respect the worker,

invite the shopper,

shout the brand’s message.

In the battle for the “First Moment of Truth,” the carton is often the deciding factor in whether a product moves from the shelf to the basket.

Would you believe that a single supermarket shelf in Poland tells the story of a massive social shift? To the uninitiated, it’s just a mix of dessert options. To an FMCG analyst, it is a roadmap of how we live, age, and eat.

“Budyń” is the Polish equivalent of English Pudding . Traditionally a warm, milk-based dessert thickened with starch, it has long been the “comfort food” of the nation. But the way we consume it is changing, reflecting a shift from the communal family table to the “on-the-go” individual.

The Three Eras

Let’s go deeper and see what was the shift that happened here.

The Traditional Ritual (The Family Pack)

You buy a 40g sachet of powder, milk, and sugar. In the kitchen, you whisk, boil, and stir. One packet yields four portions. This is the essence of old-fashion family model —a communal experience where the dessert is shared, and the labor of cleaning the pot is a small price for a family moment.

The Semi-Modern Shift (The “Cup” Revolution)

Enter the “Słodki Kubek” (Sweet Cup). You buy a smaller sachet, add boiling water and stir it directly in a coffee mug. It’s a single portion. No leftover waste, no separate pot to scrub. This was our first hint that the Polish household was shrinking.

The Hyper-Modern Reality (The Tube)

The latest evolution is the ready-to-eat pudding in a squeeze tube, like the Łowicz “à la Budyń” pictured. No kitchen, no extra ingredients, no skills, and zero cleanup. It is the ultimate “frictionless” food. You eat it on the way to the office or as a quick evening snack, and then the packaging vanishes into the bin. It’s a dessert for a life that doesn’t stop for a boiling pot.

The Demographic Engine – Why This Makes Sense

This shift isn’t just about laziness; it’s about the math of modern living. According to Eurostat, the average household size in Poland has been steadily dropping, now sitting at approximately 2.6 members, with one-person households becoming the fastest-growing segment in urban areas [Source: Eurostat, 2023]. We no longer need four portions because, increasingly, there is only one person at the table.

Another factor – The Silver Economy. Poland is one of the fastest-aging societies in the EU. By 2050, it is estimated that people aged 65 and over will make up over 30% of the population [Source: GUS].

For the elderly, the “pudding tube” is a stroke of genius. As manual abilities decreases, the struggle of holding a spoon or the danger of handling boiling milk on a stove becomes a barrier. A squeeze tube removes the risk of broken glass and the physical toll of cleaning, allowing seniors to enjoy theflavors of childhood safely and independently.

The “Daisy” Mystery

BTW – Have you noticed that almost every Cream flavored pudding features a daisy on the packaging?

What’s the business behind?

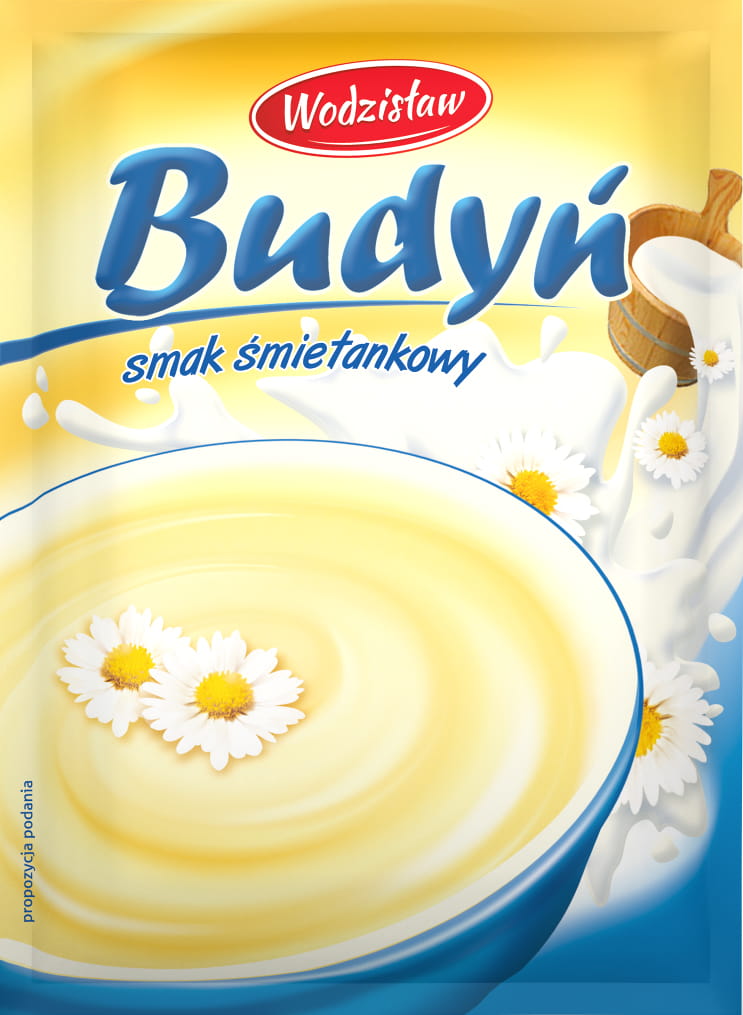

How much does that free time actually cost you? Let’s look at the financial breakdown of one portion of vanilla/cream pudding across the three formats.

Moving from the traditional pot to the modern tube increases your cost per serving by over 430%. However, in a world where a “household” is often just one busy professional or one elderly person with limited energy, the market has decided that 15 minutes of your life is worth more than the 3.24 PLN price gap.

What’s the conclusion here?

We aren’t just buying pudding anymore; we are buying the right to not have a kitchen.

We are buying the proof that in the modern world, the craving for tradition no longer requires the presence of a home.

We are buying a mess-free existence, with no more “dirty pot” era.

By choosing the squeeze tube, we trade a few extra zlotys for a dessert that requires no spoon, no bowl, and no cleanup—just pure, instant nostalgia that fits in a pocket.

You recognize the product instantly. It looks familiar. And yet something feels… off.

Yes — alternatives.

Standing in a Rossmann store in Poland, I found myself staring at a shelf that felt like déjà vu: three “healthy” snack bars, each very clearly inspired by some of the most iconic chocolate bars ever created. Snickers. Bounty. Kinder Country. Products so deeply embedded in global FMCG culture that you don’t need to read the name — your brain fills in the gaps automatically.

And that’s exactly where it gets interesting.

Case 1: Almost 1:1

In the first case, you could easily mistake one for the other.

Size: identical! Colors: same palette, same balance Graphic layout: logo placement, product shot positioning, flavor communication — all strikingly familiar Red–white contrast: matched almost perfectly

At first glance, your hand could reach out before your rational brain kicks in.

Is that inspiration — or is it already too far?

Case 2: Comparison by Design

The second example plays a slightly different game.

Here, the color coding does most of the work. The visual language immediately invites comparison between the original and the “better-for-you” version. The bar itself is similar in size, but not identical — the original is slimmer, more refined.

This is no accident. This is deliberate shelf storytelling.

Mixed Feelings — and That’s the Point

As an FMCG observer, I have mixed feelings — and that’s not necessarily a bad thing.

1

We live in a free market. Anyone can produce what they want. If consumers are buying these products, that means there is demand. Simple.

And that demand can come from at least two very different motivations:

Nostalgia with fewer regrets Consumers miss the taste and emotional comfort of classic bars but want less sugar, simpler ingredients, or better macros.

No comparison at all Some shoppers may not even consciously link the product to the original — they simply see a healthy bar that fits their needs.

In both cases, there is nothing inherently wrong. Consumers have agency. They choose.

2

But maybe there’s something more interesting happening here.

What if this copy mechanism is actually a good thing?

What if for every “bad-for-you” product, the shelf also offered a credible, healthier alternative — same flavor territory, same usage occasion, same price range?

Decision tree looks like:

You’re hungry — yes.

Do you have to buy a sugar-loaded bar — no.

Now the responsibility shifts fully to the consumer. Not because options are limited, but because options are abundant.

Imagine this logic applied consistently:

healthier versions of the most popular sweets

better-for-you alternatives to iconic savory snacks

functional substitutes that don’t feel like punishment

From a public health perspective — that’s powerful. From a brand strategy perspective — that’s disruptive.

The Numbers Behind the Icons

To understand what’s at stake, it’s worth remembering the scale of the originals:

Snickers (Mars)

One of the world’s best-selling chocolate bars

Sold in more than 70 countries

Kinder Country (Ferrero Group)

Part of a portfolio that generated €17+ billion in revenue (2023)

Kinder is among the top 5 confectionery brands globally

Especially strong in Europe, where brand trust is exceptionally high

Bounty (Mars)

A cult classic with coconut lovers worldwide

Strong emotional equity built over decades

When you “borrow” from brands of this magnitude, you’re not just borrowing design — you’re tapping into decades of mental availability built with billions in advertising spend. ANd here comes the question:

Inspiration vs. Imitation: Where Is the Line?

And this brings us to the uncomfortable but necessary question:

Where is the real border between inspiration and copying?

Is it the flavor combination? The packaging design? The color system? The overall “look & feel” at shelf distance?

There is no universal formula — only context, intention, and consumer perception.

And perhaps that’s the most fascinating part.

Because in the end, the shelf doesn’t ask for legal arguments. It asks one simple question:

Which bar will the consumer pick — and why?

And increasingly, the answer may be:

“The one that feels familiar… but makes me feel better about myself.”